Scope 3 Inventory Guidance

On this page:

- Description of Scope 3 Emissions

- Scope 3 Calculation: Practical Guidance

- Supply Chain Guidance

- Scope 3 Emission Factors

- Scope 3 Resources

Description of Scope 3 Emissions

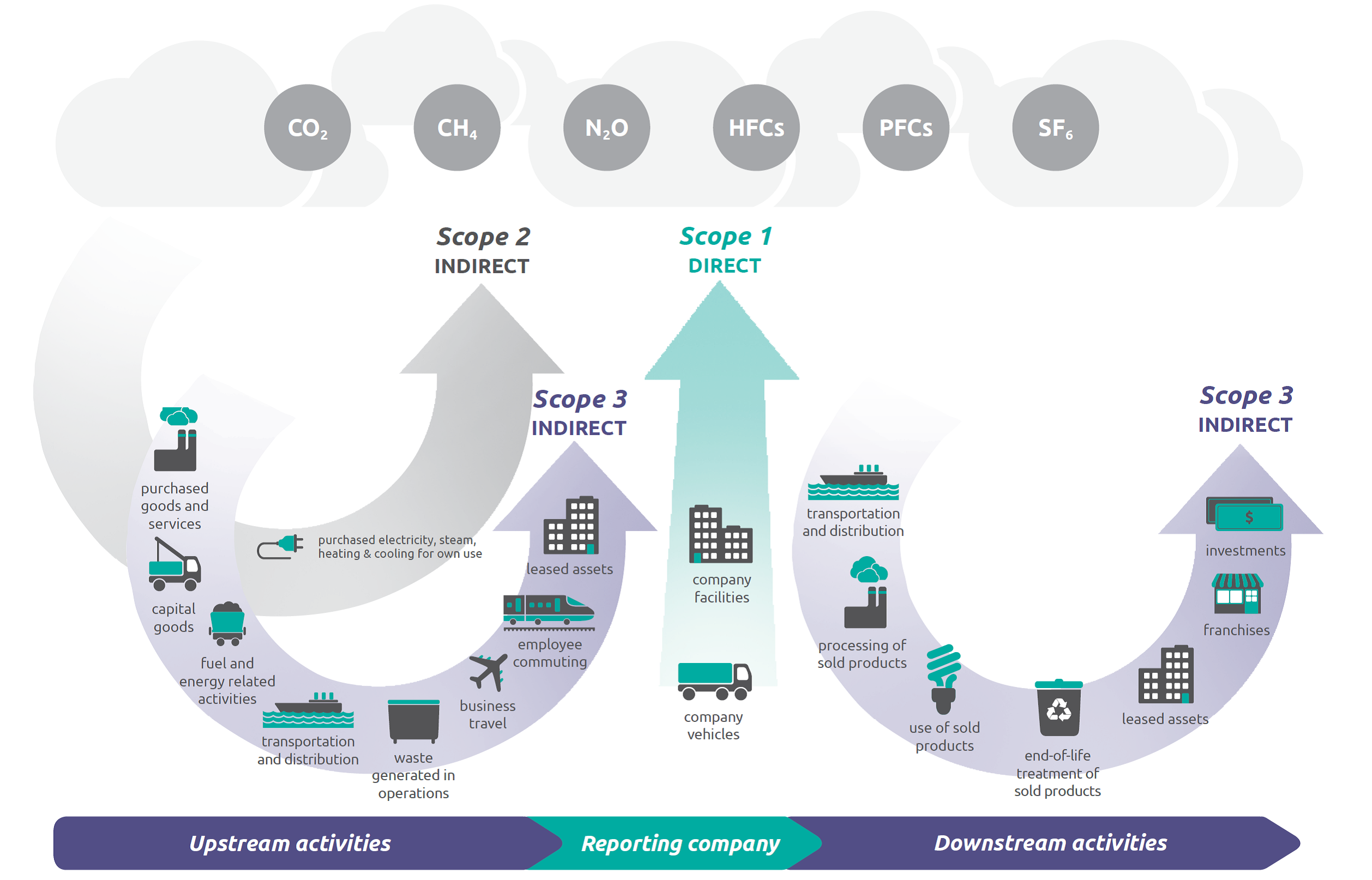

Scope 3 emissions are the result of activities from assets not owned or controlled by the reporting organization, but that the organization indirectly affects in its value chain. An organization’s value chain consists of both its upstream and downstream activities. Scope 3 emissions include all sources not within an organization’s scope 1 and 2 boundary. The scope 3 emissions for one organization are the scope 1 and 2 emissions of another organization. Scope 3 emissions, also referred to as value chain emissions, often represent the majority of an organization’s total greenhouse gas (GHG) emissions.

The GHG Protocol defines 15 categories of scope 3 emissions, though not every category will be relevant to all organizations (see Figure 1). Scope 3 emission sources include emissions both upstream and downstream of the organization’s activities.

To fully meet GHG Protocol standards, an organization must report emissions from all relevant scope 3 categories. More organizations are reaching into their value chains to understand the full GHG impact of their operations. In addition, because scope 3 sources may represent most of an organization’s GHG emissions, they often offer emissions reduction opportunities. Although these emissions are not under the organization’s control, the organization may be able to affect the activities that result in the emissions. The organization may also be able to influence its suppliers or choose which vendors to contract with based on their practices.

The GHG Protocol's Corporate Value Chain (Scope 3) Accounting and Reporting Standard (“Scope 3 Standard”) presents details on all scope 3 categories and requirements and guidance on reporting scope 3 emissions.

Figure 1. Overview of GHG Protocol scopes and emissions across the value chain

Scope 3 Calculation: Practical Guidance

The Scope 3 Standard (pdf) (5.9 MB) presents details on all scope 3 categories and requirements and guidance on reporting scope 3 emissions. The practical guidance below provides further suggestions on calculating scope 3 emissions.

Establishing a relevant, complete, consistent, transparent, and accurate scope 3 emissions inventory is a process of continuous improvement. Table 1 provides a description of organizational phases of scope 3 engagement for common inventorying best practices. For some organizations, understanding GHG inventorying efforts within the broader market may spur competition and garner internal support for widening inventorying activities.

| Stage | Does your company calculate and publicly disclose at least some scope 3 emissions? | Does your company assess the climate impacts of major suppliers and engage them on climate-related issues? | Does your company receive third-party verification for its scope 3 emissions and publicly disclose the results? |

|---|---|---|---|

| No activity | Organization does not calculate and publicly disclose any scope 3 emissions. | Organization does not assess the climate impacts (both actual and significant potential impacts) of major suppliers or engage them on climate-related issues. | Organization does not receive third-party verification for its scope 3 emissions or publicly disclose the results. |

| Entry-level | Organization calculates and publicly discloses at least some scope 3 emissions. | Organization assesses the climate impacts (both actual and significant potential impacts) of major suppliers and engages them on climate-related issues. | Organization receives third-party verification for a portion of its scope 3 emissions and publicly discloses the results. |

| Intermediate | Organization calculates and publicly discloses more than two categories of scope 3 emissions that are considered relevant in their value chain. | Organization assesses the climate impacts (both actual and significant potential impacts) of their major suppliers and engages them to report and reduce their GHG emissions. | Organization receives third-party verification for all its scope 3 emissions and publicly discloses the results. |

| Advanced | Organization calculates and publicly discloses all relevant categories of scope 3 emissions. | Organization assesses the climate impacts (both actual and significant potential impacts) of their major suppliers, engages them to report and reduce their GHG emissions, and considers supplier GHG management in business decisions. | Organization receives third-party verification for all its scope 3 emissions to at least a level of limited assurance and publicly discloses results. |

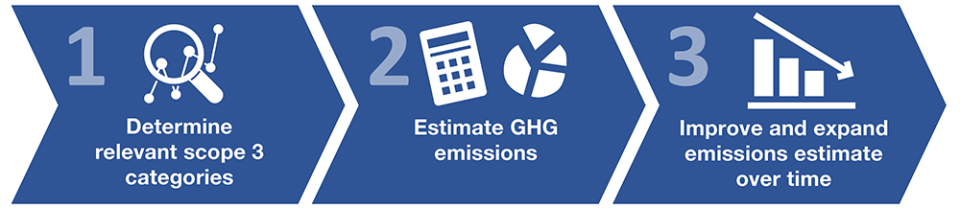

Quantifying scope 3 emissions can be broken into three steps:

Step 1: Determine relevant scope 3 categories

The first step is a relevance assessment to determine which of the 15 categories are relevant to the reporting organization. Table 6.1 of the Scope 3 Standard (pdf) (5.9 MB) provides criteria to identify relevant scope 3 activities:

- Size

- Influence

- Risk

- Stakeholders

- Outsourcing

- Sector guidance

- Other

To determine relevance, the organization can review the Scope 3 Standard’s description of each scope 3 category and consult appropriate contacts across the organization. In some cases, an emissions estimate may be necessary to determine if the category is relevant based on size. A rough estimate will suffice, but if that is not possible, then proceed to step 2 to estimate emissions.

Step 2: Estimate GHG emissions

Estimates for scope 3 categories can vary in accuracy depending on the available data and the organization’s quantification goal. For example, category 4 (upstream transportation and distribution) has three methods: fuel-based, distance-based, and spend-based. The GHG Emission Factors Hub provides factors for several scope 3 categories and indicates the calculation methods with which the factors align. For example, Table 8 of the GHG Emission Factors Hub lists factors aligned with the distance-based method. If fuel activity data are available, the fuel-based method should be used, so the factors presented in Tables 2 and 3 would be applicable. See the “Scope 3 Emission Factors” section below for more details.

The GHG Protocol provides Scope 3 Calculation Guidance which details multiple calculation methods for each scope 3 category based on level of specificity and available data.

For financial institutions, The Global GHG Accounting and Reporting Standard for the Financial Industry (pdf) (10.2 MB), published by the Partnership for Carbon Accounting Financials, offers specific guidance on calculating scope 3, category 15 (investments) emissions.

Step 3: Improve and expand emissions estimate over time

Many organizations will improve the accuracy of scope 3 emissions over time and expand to include more categories as adequate data become available.

Improve

- More accurate data sources. This could include moving from secondary sources to primary ones. For example, in the first year of reporting, an organization may only be able to track spend for business travel, but in subsequent years, miles traveled by type (air, rail, car) may be available.

- More specific calculation methods. It is appropriate to use a combination of calculation methods within a category (for example, collecting supplier emissions data for high emissions suppliers and estimating based on spend for the remaining suppliers). However, these methods should remain consistent for year-over-year comparison; any change in method used will require historical adjustments (see Chapter 9 of the Scope 3 Standard).

Expand

Some scope 3 categories may be relevant, but initially lack readily available data to use in estimating emissions. The organization may be able to expand its reporting by estimating these relevant categories in the future, which is recommended to increase completeness.

When making these improvements, it is recommended to focus first on categories with the largest impact on the organization’s total GHG inventory.

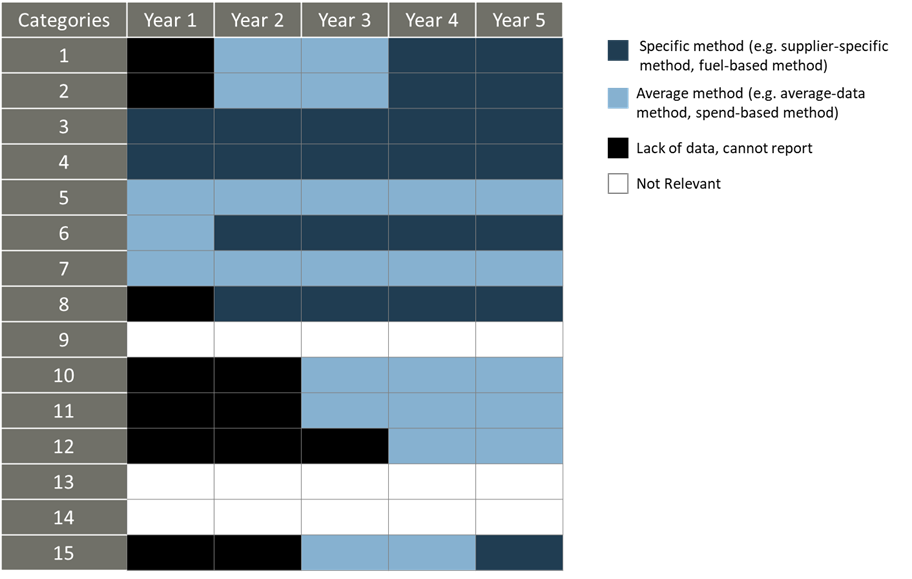

Figure 2 shows an example progression over time of improvement and expansion. Five categories are reported in year one and 12 in year five. Only two categories use a specific method (e.g., supplier-specific method, fuel-based method) in year one and seven in year five.

Figure 2. Scope 3 calculation method improved and boundary expanded over time

Supply Chain Guidance

An organization’s supply chain comprises its upstream activities (see Figure 1). Organizations' supply chains emissions are, on average, 11.4 times higher than operational emissions, which equates to approximately 92% of an organization's total GHG emissions (Source: CDP 2020 Global Supply Chain Report (pdf) (4.2 MB)).

EPA’s supply chain guidance provides information on:

- Why engage suppliers?

- How to engage suppliers.

- Building internal support in supply chain management.

- Leveraging third-party programs.

- Examples of sector-specific engagement.

- Resources for reducing supply chain emissions.

Scope 3 Emission Factors

Table 2 shows EPA's recommended source of emission factors for each scope 3 category. The most common sources listed in the table are:

- EPA's USEEIO supply chain GHG emission factors are based on US Environmentally-Extended Input-Output models and are presented in emissions per dollar of spend.

- EPA's GHG Emission Factors Hub provides factors for most scope 3 categories. Some categories do not require specific emission factors, because the emissions-generating activities have associated scope 1 and scope 2 factors already available.

| Scope 3 Category | Emission Factor Source |

|---|---|

| 1 (purchased goods and services) | USEEIO |

| 2 (capital goods) | USEEIO |

| 3 (fuel- and energy-related activities) |

Activity A. Upstream emissions of purchased fuels The UK Department for Environment Food & Rural Affairs provides well-to-tank (i.e., upstream) emission factors for fuel in the "Conversion factors 2023: full set (for advanced users)" spreadsheet (on the "WTT- fuels" worksheet). Activity B. Upstream emissions of purchased electricity

Activity C. Transmission and distribution (T&D) losses US: International:

Activity D. Generation of purchased electricity that is sold to end users |

| 4 (upstream transportation and distribution) | EF Hub, Table 8 |

| 5 (waste generated in operations) | EF Hub, Table 9 |

| 6 (business travel) | EF Hub, Table 10 |

| 7 (employee commuting) | |

| 8 (upstream leased assets) | EF Hub; apply scope 1 and 2 factors |

| 9 (downstream transportation and distribution) | EF Hub, Table 8 |

| 10 (processing of sold products) | EF Hub; apply scope 1 and 2 factors |

| 11 (use of sold products) | |

| 12 (end-of-life treatment of sold products) | EF Hub, Table 9 |

| 13 (downstream leased assets) | EF Hub; apply scope 1 and 2 factors |

| 14 (franchises) | |

| 15 (investments) |

To apply the EF Hub scope 1 and 2 factors, the organization can first define the GHG generating activity for each relevant source category, then apply the appropriate factors for stationary combustion, mobile combustion, fugitive emissions, electricity, heat, or steam.

For example, if an organization produces electronic equipment, Category 11 (use of sold products) may likely be a large source of emissions. To calculate emissions, estimate the lifetime electricity consumption (in kWh) for all products sold in the reporting year. Then calculate electricity emissions using emission factors in the EF Hub. Depending on the data available for the location of product use, apply eGRID subregion or U.S. national average factors.

Scope 3 Resources

Standards and Guidance

- Renewable Electricity Procurement on Behalf of Others: A Corporate Reporting Guide (pdf) is a U.S. practice paper focused on key principles for procuring renewable electricity on behalf of value chain partners and provides examples for several procurement scenarios. It aligns with the principles of the GHG Protocol Scope 2 Guidance for renewable electricity procurement within a reporting entity's value chain.

- Renewable Electricity Procurement for Use of Sold Products (pdf) is a U.S. practice paper that discusses how renewable electricity procurement may help reporting organizations reduce their scope 3, category 11 GHG emissions that result from the use of sold products that consume electricity.

- Indirect Emissions from Events and Conferences (pdf) covers indirect emissions—including emissions from travel, hotel stays, and the venue itself—for events (e.g., sporting events, concerts) and conferences (e.g., business meetings, exhibits, conventions).

Tools

- ENERGY STAR Scope 3 Use of Sold Products Analysis Tool V2.0 (November 2023) (xlsm) allows retailers to benchmark and project corporate scope 3 GHG emissions associated with the use of sold products. Developed jointly with EPA's Center for Corporate Climate Leadership, this tool quantifies emissions associated with current sales of ENERGY STAR products and forecasts reductions in emissions based on increases in sales of ENERGY STAR products. With over 70 categories, it can help retailers of any size pinpoint the types and quantities of ENERGY STAR products that will bring them closer to meeting or beating their corporate carbon emission goals.